If you run a Malaysian business, there is a good chance your books already live in Bukku accounting. It is homegrown, LHDN e-invoice ready, and built for exactly the kind of business you run. What Bukku does not do on its own is chase down the receipt, remember which card paid for it, or stop an employee from expensing something they should not have.

That gap, between money leaving the business and money landing correctly in Bukku, is where most finance teams still lose their week. Here is what that gap actually costs, and how to close it.

What Bukku accounting actually does well

Bukku is a cloud accounting platform built specifically for Malaysian SMEs, invoicing, bank reconciliation, inventory, SST reporting, and fixed asset depreciation, without needing an accounting background to run it. It is also one of the few platforms with LHDN e-invoicing built in on every plan, submitting to MyInvois in a click and connecting to the Peppol network as an accredited service provider.

That is exactly why it is the system of record for a large share of Malaysian SMEs and the accounting firms that serve them. But a system of record is only as good as what feeds it. Bukku accounting can tell you what happened to your money once the transaction is entered, it does not stop the transaction from happening the wrong way, and it does not enter itself.

The part between spending and Bukku is still manual for most businesses

Walk through a typical month: an employee pays for a Google Ads top-up on a personal card, a subscription renews on the founder’s card, a supplier gets paid by bank transfer, and a petrol receipt sits in someone’s glove box until month-end. Every one of those has to be tracked down, categorised, and keyed into Bukku by hand before your books are actually accurate.

This is the piece a card platform is supposed to solve, and it is also where most card platforms stop short. Corporate card providers built for Singapore or cross-border spend, like Airwallex, sync natively into Xero, QuickBooks and NetSuite. None of them currently sync into Bukku, so if Bukku is your system of record, that data still has to be exported, reformatted, and re-entered. For a market where Bukku is one of the default choices, that is a real gap.

How Swipey closes the loop into Bukku accounting

Why this matters more in 2026: Bukku accounting and MyInvois

Malaysia’s e-invoicing mandate is no longer a future problem. Businesses with turnover above RM5 million have been submitting to LHDN’s MyInvois system since mid-2025, and the next band, turnover between RM1 million and RM5 million, came into scope from 1 January 2026 with a 12-month relaxation period. Bukku is built for this: e-invoicing is included on every plan and submissions go to MyInvois in a click through its Peppol-accredited connection.

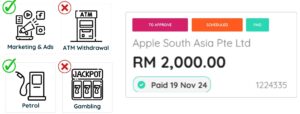

E-invoicing compliance only works if the underlying spend data feeding Bukku is accurate and complete in the first place, which is the half of the problem card platforms are meant to solve. Swipey adds per-card spend limits, no shared OTPs or logins, merchant category restrictions, and a full audit trail on top of a Bukku ledger, so the same records that go out to LHDN also hold up if your own auditor or bank comes asking questions.

Why most corporate cards leave Bukku users doing it manually

Cross-border platforms like Airwallex are genuinely good at what they are built for, and they integrate with Xero, QuickBooks and NetSuite to prove it. None of them currently connect to Bukku. If your accountant already works in Bukku, which is likely if you are a Malaysian SME, switching your spend platform to one of these means either moving your books off Bukku or exporting and re-importing data by hand every month. Swipey syncs into Bukku natively, so you keep the accounting system your bookkeeper already knows.

Your books, done automatically in Bukku

Card swiped, receipt captured, category mapped, synced to Bukku, books closed. No manual entry, no month-end scramble.